Optimization would not work , backtesting is working

Optimization would not work , backtesting is working

26 Feb 2018, 11:01

using System;

using System.Linq;

using cAlgo.API;

using cAlgo.API.Indicators;

using cAlgo.API.Internals;

using cAlgo.Indicators;

namespace cAlgo

{

[Robot(TimeZone = TimeZones.RussianStandardTime, AccessRights = AccessRights.FullAccess)]

public class Donci3Av7 : Robot

{

#region Parameters

[Parameter("Instance Name", DefaultValue = "Blue")]

public string InstanceName { get; set; }

[Parameter()]

public DataSeries Source { get; set; }

[Parameter("Time Frame 2", DefaultValue = "Daily")]

public TimeFrame TimeFrame2 { get; set; }

[Parameter("Time Frame 3", DefaultValue = "Hour12")]

public TimeFrame TimeFrame3 { get; set; }

[Parameter("SL ATR multiple", DefaultValue = 2.2)]

public double ATRfactor { get; set; }

[Parameter("Hi Periods", DefaultValue = 20, MinValue =15, MaxValue =40, Step =1)]

public int HiPer { get; set; }

[Parameter("Low Periods", DefaultValue = 10, MinValue = 5, MaxValue =30, Step =1)]

public int LowPer { get; set; }

[Parameter("Quantity (Lots)", DefaultValue = 0.1, MinValue = 0.01, Step = 0.01)]

public double Quantity { get; set; }

[Parameter("Include Trading Hours", DefaultValue = false)]

public bool IncludeTradinHours { get; set; }

[Parameter("Start Hour", DefaultValue = 0.0, MinValue = 0.0, MaxValue = 24.0, Step = 0.5)]

public double StartTime { get; set; }

[Parameter("Stop Hour", DefaultValue = 24.0, MinValue = 0.0, MaxValue = 24.0, Step = 0.5)]

public double StopTime { get; set; }

[Parameter("Include Break-Even", DefaultValue = true)]

public bool IncludeBreakEven { get; set; }

[Parameter("Break-Even Trigger (SL)", DefaultValue = 1, MinValue = 0.4, MaxValue = 4.0)]

public double Trigger { get; set; }

[Parameter("Break-Even Extra (pips)", DefaultValue = 1.0, MinValue = 0.0)]

public double ExtraPips { get; set; }

[Parameter("Include Trailing Stop", DefaultValue = true)]

public bool IncludeTrailingStop { get; set; }

[Parameter("Trailing Stop Trigger (SL)", DefaultValue = 1.5, MinValue = 0.3, Step = 0.1)]

public double TrailingStopTrigger { get; set; }

[Parameter("Trailing Stop Step (SL)", DefaultValue = 1.2, MinValue = 0.1, Step = 0.1)]

public double TrailingStopStep { get; set; }

[Parameter("Max Spread (Pips)", DefaultValue = 2.0, MaxValue = 50.0, Step = 0.1)]

public double MaxSpread { get; set; }

private DateTime _startTime;

private DateTime _stopTime;

private double ma_Distance;

private MarketSeries series2;

private MarketSeries series3;

private MovingAverage MA2;

private MovingAverage MA3;

private MovingAverage MA;

private string _Blue;

public double SL;

private double _ATR;

private DonchianChannel DCH;

private DonchianChannel DCL;

private AverageTrueRange ATR;

private TradeType _tradetype;

private bool BuyTradeOK;

private bool SellTradeOK;

#endregion

#region OnStart

protected override void OnStart()

{

// Start Time is the same day at 22:00:00 Server Time

_startTime = Server.Time.Date.AddHours(StartTime);

// Stop Time is the next day at 06:00:00

_stopTime = Server.Time.Date.AddHours(StopTime);

Print("Start Time {0},", _startTime);

Print("Stop Time {0},", _stopTime);

ma_Distance = 0.2;

ma_Distance = ma_Distance * Symbol.PipSize;

series2 = MarketData.GetSeries(TimeFrame2);

series3 = MarketData.GetSeries(TimeFrame3);

MA = Indicators.MovingAverage(Source, HiPer, MovingAverageType.Exponential);

MA2 = Indicators.MovingAverage(series2.Close, HiPer, MovingAverageType.Exponential);

MA3 = Indicators.MovingAverage(series3.Close, HiPer, MovingAverageType.Exponential);

_Blue = "Donci 3Av7 " + "Blue" + " " + Symbol.Code;

InstanceName = _Blue;

ATR = Indicators.AverageTrueRange(LowPer, MovingAverageType.Exponential);

SL = ATR.Result.LastValue * ATRfactor / Symbol.PipSize;

DCH = Indicators.DonchianChannel(HiPer);

DCL = Indicators.DonchianChannel(LowPer);

_ATR = ATR.Result.LastValue;

}

#endregion

#region OnTick

protected override void OnTick()

{

if (IncludeTradinHours)

{

var currentHours = Server.Time.TimeOfDay.TotalHours;

bool tradeTime = StartTime < StopTime ? currentHours > StartTime && currentHours < StopTime : currentHours < StopTime || currentHours > StartTime;

if (!tradeTime)

return;

}

var position = Positions.Find(InstanceName, Symbol);

if (position == null)

{

if (MA2.Result.LastValue < Symbol.Bid - ma_Distance && MA3.Result.LastValue < Symbol.Bid - ma_Distance && MA2.Result.IsRising() && MA3.Result.IsRising() && Symbol.Spread <= MaxSpread)

{

BuyTradeOK = true;

SellTradeOK = false;

}

if (MA2.Result.LastValue > Symbol.Ask + ma_Distance && MA3.Result.LastValue > Symbol.Ask + ma_Distance && MA2.Result.IsFalling() && MA3.Result.IsFalling() && Symbol.Spread <= MaxSpread)

{

BuyTradeOK = false;

SellTradeOK = true;

}

if ((DCH.Top.LastValue < Symbol.Bid && BuyTradeOK) || (DCH.Bottom.LastValue > Symbol.Bid && SellTradeOK))

{

_tradetype = BuyTradeOK ? TradeType.Buy : TradeType.Sell;

Open(_tradetype);

}

}

else if (position != null)

{

if ((position.TradeType == TradeType.Buy && DCL.Bottom.LastValue > Symbol.Bid) || (position.TradeType == TradeType.Sell && DCL.Top.LastValue < Symbol.Bid))

{

ClosePosition(position);

}

}

if (IncludeBreakEven == true)

GoToBreakEven();

if (IncludeTrailingStop == true)

SetTrailingStop();

}

#endregion

#region Open trade

void Open(TradeType tradeType)

{

var volumeInUnits = Symbol.QuantityToVolume(Quantity);

SL = ATR.Result.LastValue * ATRfactor / Symbol.PipSize;

ExecuteMarketOrder(tradeType, Symbol, volumeInUnits, InstanceName, SL, null);

}

#endregion

#region Break Even

void GoToBreakEven()

{

var position = Positions.Find(InstanceName, Symbol);

if (position != null)

{

var entryPrice = position.EntryPrice;

var distance = 0.0;

var adjEntryPrice = 0.0;

if (position.TradeType == TradeType.Buy)

{

adjEntryPrice = entryPrice + ExtraPips * Symbol.PipSize;

distance = Symbol.Bid - entryPrice;

}

else

{

adjEntryPrice = entryPrice - ExtraPips * Symbol.PipSize;

distance = entryPrice - Symbol.Ask;

}

if (distance >= Trigger * SL * Symbol.PipSize)

{

if (position.TradeType == TradeType.Sell && position.StopLoss > adjEntryPrice)

ModifyPosition(position, adjEntryPrice, null);

if (position.TradeType == TradeType.Buy && position.StopLoss < adjEntryPrice)

ModifyPosition(position, adjEntryPrice, null);

}

}

}

#endregion

#region Trailing Stop

private void SetTrailingStop()

{

var sellPositions = Positions.FindAll(InstanceName, Symbol, TradeType.Sell);

foreach (Position position in sellPositions)

{

double distance = position.EntryPrice - Symbol.Ask;

if (distance < TrailingStopTrigger * SL * Symbol.PipSize)

continue;

double newStopLossPrice = Symbol.Ask + TrailingStopStep * SL * Symbol.PipSize;

if (position.StopLoss == null || newStopLossPrice < position.StopLoss)

{

ModifyPosition(position, newStopLossPrice, position.TakeProfit);

}

}

var buyPositions = Positions.FindAll(InstanceName, Symbol, TradeType.Buy);

foreach (Position position in buyPositions)

{

double distance = Symbol.Bid - position.EntryPrice;

if (distance < TrailingStopTrigger * SL * Symbol.PipSize)

continue;

double newStopLossPrice = Symbol.Bid - TrailingStopStep * SL * Symbol.PipSize;

if (position.StopLoss == null || newStopLossPrice > position.StopLoss)

{

ModifyPosition(position, newStopLossPrice, position.TakeProfit);

}

}

}

#endregion

}

}

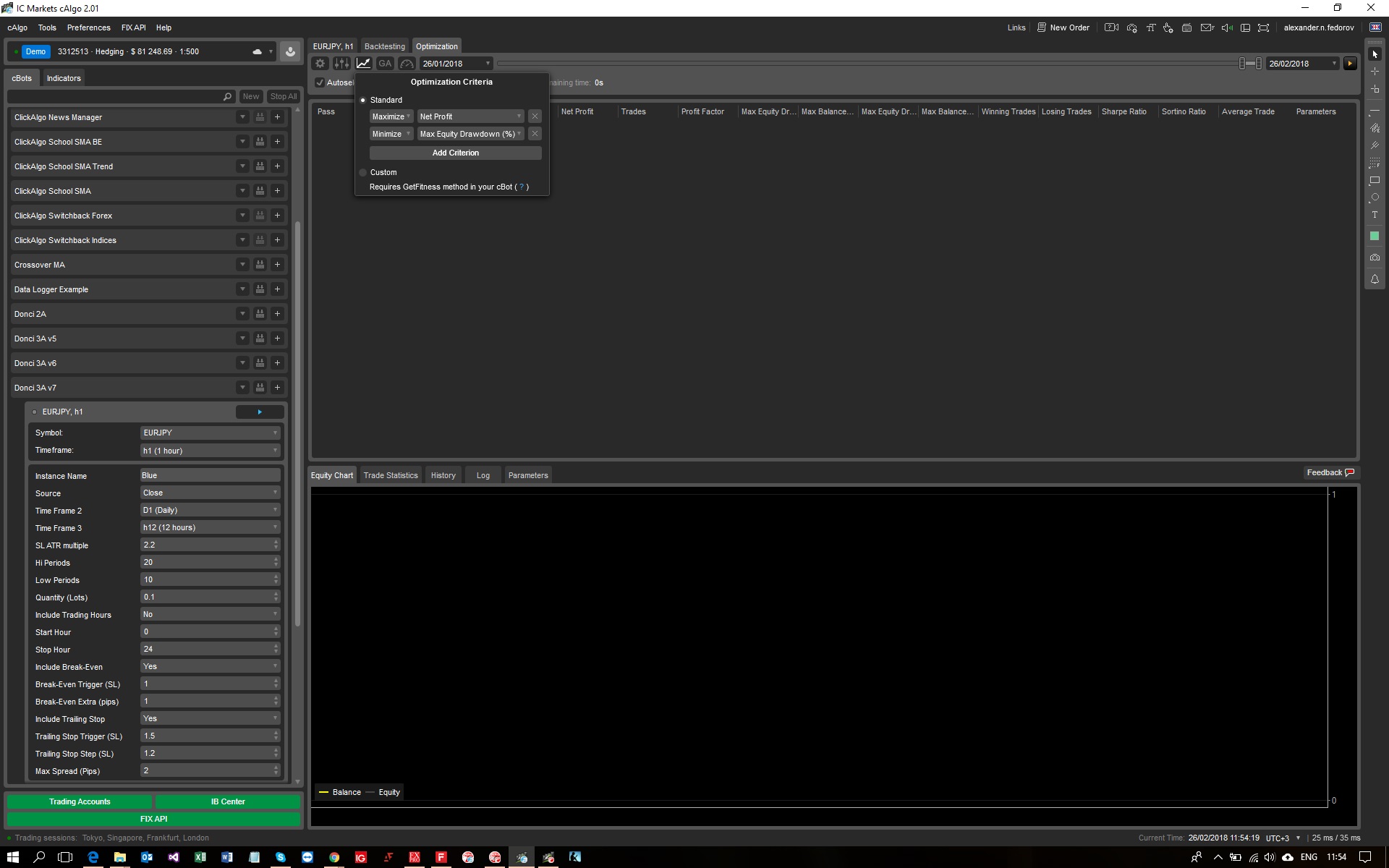

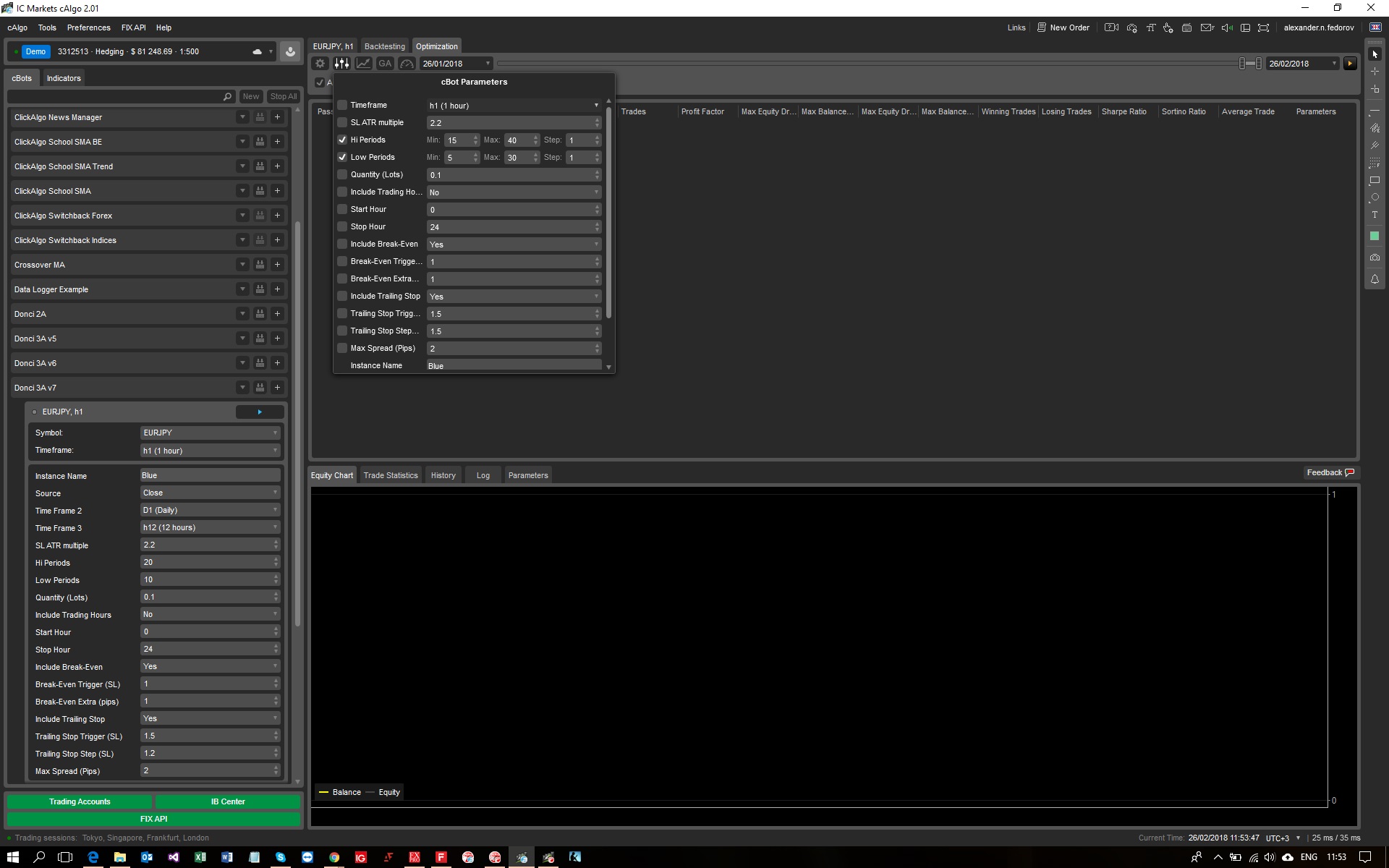

I will try to add the screens

Replies

alexander.n.fedorov

26 Feb 2018, 11:58

Backtesting

The funny thing is that I did not change anything on both computers, and all of a sudden optimization is woking OK now.

What could it possibly be?

@alexander.n.fedorov

PanagiotisCharalampous

26 Feb 2018, 12:21

Hi Alexander,

It is not clear what was the problem. What do you mean that optimization was not working?

Best Regards,

Panagiotis

@PanagiotisCharalampous

alexander.n.fedorov

26 Feb 2018, 12:50

Hi, Panagiotis,

it starts, and after few seconds it stops with remaining time 0 seconds

I tryied to drop the *.png screenshot files, or *.jpg, but also could not do much, as it was taking the whole screen. How do I upload a jpg file?

@alexander.n.fedorov

alexander.n.fedorov

26 Feb 2018, 12:52

Backtesting

If you could send me your skype or e-mail,

I could send you the screenshots

just in case my skype is alexander.n.fedorov

and mail is alexander.n.fedorov@gmail.com

@alexander.n.fedorov

PanagiotisCharalampous

26 Feb 2018, 12:53

( Updated at: 19 Mar 2025, 08:57 )

Hi Alexander,

There is an image button when you are creating the post, use that. Else send the screenshots to support@ctrader.com. Also sending the cBot would be helpful so that we can reproduce the problem.

Best Regards,

Panagiotis

@PanagiotisCharalampous

alexander.n.fedorov

26 Feb 2018, 12:55

Backtesting

the Bot code is up the screen

I will try the image button again

@alexander.n.fedorov

alexander.n.fedorov

26 Feb 2018, 13:16

Backtesting

Panagiotis,

I tryied to do it on two differen computers. On both it did not work

Now it is working on both.

Out of that I think it was something with a server connection.

Alexander

@alexander.n.fedorov

alexander.n.fedorov

26 Feb 2018, 11:11

How do you add the screenshots?

I did not figure out how to post the screens.

@alexander.n.fedorov